Oil and gas incumbents are doubling down on investment and their financial backers are exiting governance bodies: this raises the risks to investors to another level as new energy technologies enter at scale and speed.

In 2018 The Onion a satirical US magazine had the following headline:

ExxonMobil CEO depressed after realizing earth could end before they finish extracting all the oil.

That CEO was Darren Woods, and today, six years later, he is still Exxon CEO, and he is still extolling the need for increased oil and gas production.

Never a truer word spoken in jest as the bard Shakespeare noted. Whatever laughter we may have had at the time is now even more hollow. Such is the essence of satire.

But a longer reality endures: fossil fuels and their emissions are a universal waste of energy, whatever Mr Woods’ personal ideas may be.

Let’s be more precise: about 67% of all fossil fuels used are lost to the atmosphere as carbon dioxide, other oxides, and water vapour.

Only the remaining 33% is actually used to power things, transport things and heat things.

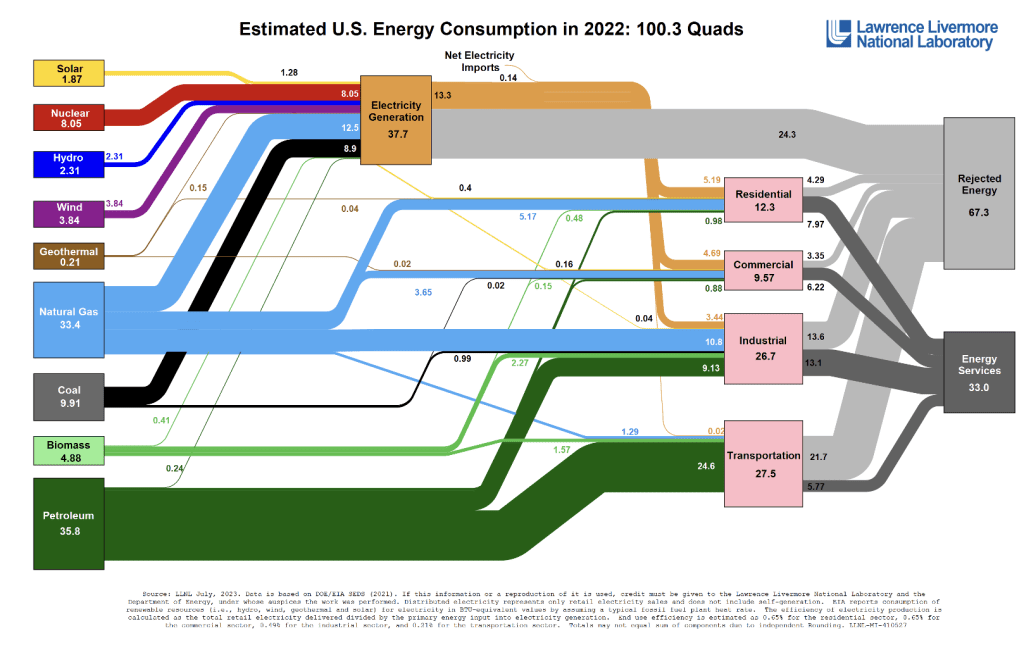

The flowchart below from the Lawrence Livermore National Laboratory puts it graphically in the context of the US – but the picture is global. For all its detail, just focus of the right hand side and the “rejected energy” number at 67%. And that is before all the losses in between, from extraction in distant oil fields to shipping vessels, refineries and gasoline trucks are factored in.

(Technical point: a “quad” in the diagram below is equal to 1 exajoule, and the world uses 600 exajoules per year, so the US uses 17% of global energy ie 100 exajoules. Note – it consumes 100 exajoules, but it only “needs” 33 exajoules – a point worth keeping in mind for this blog and foreshadowing many others to come as the world energy system moves away from fossil fuels to more efficient systems – ie peak energy may now be here).

Such a wasteful (and harmful) energy system is therefore hugely uneconomic, and only remains a core part of global energy due to limited competition (historically), and the cartel behaviour of OPEC propping up prices via production cuts whenever prices fall.

The Paris COP of 2015 placed 1.5 degC on the world energy agenda, and various initiatives on the back of it raised the spectre of reducing emissions as necessary to mitigate climate impact.

This helped usher in non-fossil fuel technologies at scale: wind, solar, batteries, EVs and modular heat technologies.

As of 2023, wind and solar alone outspent upstream oil and gas capital at $650 billion per year versus oil and gas expenditure of $480bn, and they account for 15% of global power. Electric cars account for one in six of new sales globally, growing at 35% per annum.

There is now a vast new energy system emerging at scale that can challenge fossil fuels on multiple fronts. We are now entering an era of energy surplus.

Investors and stakeholders should hold on to these basic economics, physics and chemistry facts and prick up their ears to any move by these incumbents (oil and gas companies and their backers) to plunge further into over-building the existing fossil fuel system.

At Carbon Tracker we have compressed all of this argumentation into the phrase “stranded assets”.

And yet despite years of this counsel and caution, we see the incumbent fossil fuel industry engage in more careless investments. More recently lead by ideology rather than investment logic.

Incumbents are doubling down in fossil fuel investment and slipping free from oversight

Recent news in the energy industry suggests that incumbents are doubling down into further fossil fuel investments, raising the risk of stranding their assets in a disordered way.

They do this directly by over-investing in fixed assets that are not required: a subject we covered in detail last year eg in Navigating Peak Demand, and as noted by the IEA in various reports dating back to 2021 indicating no new investments in oil and gas production are necessary as oil demand peaks, and new energy systems arrive to fill any gaps.

And they also do so indirectly by relying on investment banks and political supporters retreating from external governance and oversight initiatives such as CA100+ which aims to engage with oil and gas firms to support goals to reduce emissions and increase transparency on climate action financial disclosures.

We covered this in a CA 100+ report late last year and showed that many of their Net Zero targets are not being met or remain vague and we have an update here for oil and gas firms and here for utility companies.

As the oil and gas Carbon Tracker CA 100+ analysis notes, Despite the IEA’s unequivocal statements about there being no need for new oil and gas projects, we continue to see investments in new upstream oil and gas projects that, on a cost basis, are inconsistent with both the Net Zero Emissions by 2050 Scenario (NZE) and even the less stringent Announced Pledges Scenario (APS).

We also analysed three major utility companies in Europe this month , Snam, Enagas and Italgas and noted that their targets for net zero remain uncertain and that goals beyond 2030 seem to lack depth.

Key questions we raised were

- How far gas network operators are Paris aligned.

- How realistic is decarbonisation with hydrogen.

- Whether asset lives are appropriate with lower gas demand and net zero.

- Whether regulators are sufficiently focused on decarbonisation.

- Above all, the future of gas networks in a world increasingly dominated by renewables & electrification.

Incumbents still looking to business as usual, and even growth

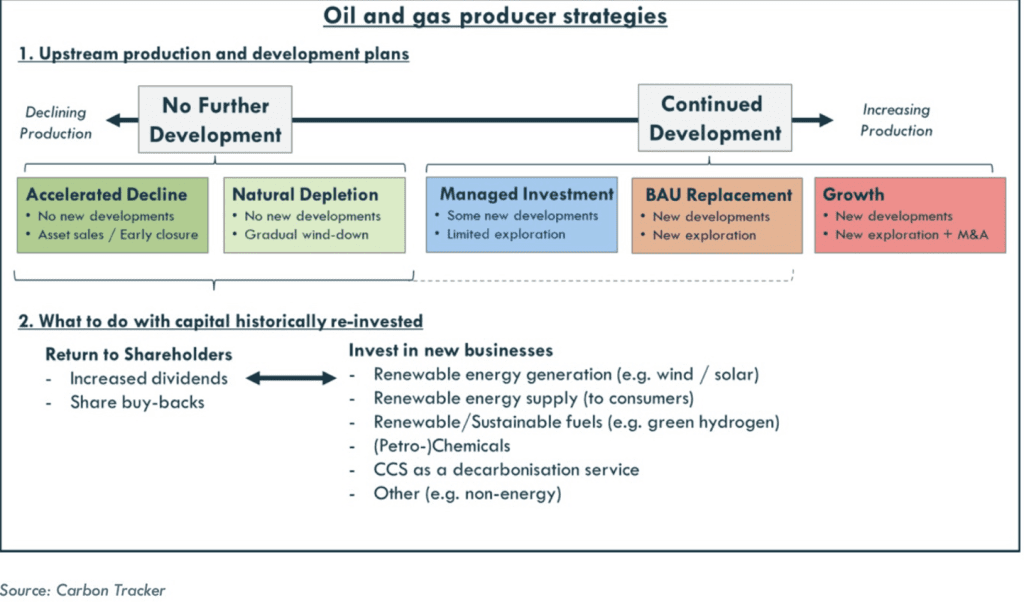

In the CT Navigating Peak Demand Report we outline several routes to reduce exposure to oil and gas decline by incumbents, for example, no further development (managed exit and accelerated decline) or limited development with managed investment, or just replacements of existing production. See the diagram below.

But still oil and gas companies look to the far edge of options to focus on growth – see the statements of Total’s CEO this month.

International oil company investments in new energy technologies amount to less than 3% of capital expenditure: the rest going into fossil fuel projects or ongoing operational maintenance, and increasingly into financial options such as share buy-backs, increased dividends and debt restructuring.

This is ironic given that even OPEC has recognised the need to pull back production as fossil fuel demand growth slows to a halt.

An exit from discipline

In line with the limited effort of transforming to new energy options, oil and gas firms and their capital backers have started to exit from low-emissions governance forums.

This has culminated in the past few weeks with four major investment firms, Pimco, Blackrock, State Street and JP Morgan withdrawing from the CA100+ initiative – removing over $14 trillion of funds or 20% of the commitment at a stroke.

This may be politically motivated in a US election year, as the article notes.

Or the CA100+ withdrawal may derive from cold logic contrarian thinking, pushing back at zero emissions fads.

But going back to our view that emissions equate to waste and economic inefficiency, this logic however prompted is actually the opposite of good corporate governance.

It is more emotional, a plunge into business risk just at the point that a more efficient energy system emerges at scale and pace.

The more genuine cold logic is that emissions are risky for the planet, yes. – but very risky for today’s business, no matter the desires of Exxon’s CEO or the financial firms stepping back from the likes of CA100+ discipline.

To remind: energy emissions are waste and inefficient. To invest in them is investing in, well inefficiency and waste.

Stakeholders should start to raise the view that continued fossil fuel investments coupled with exit from governance bodies is a sign of business frailty and inefficiency, not a new hard-edged investment strategy.

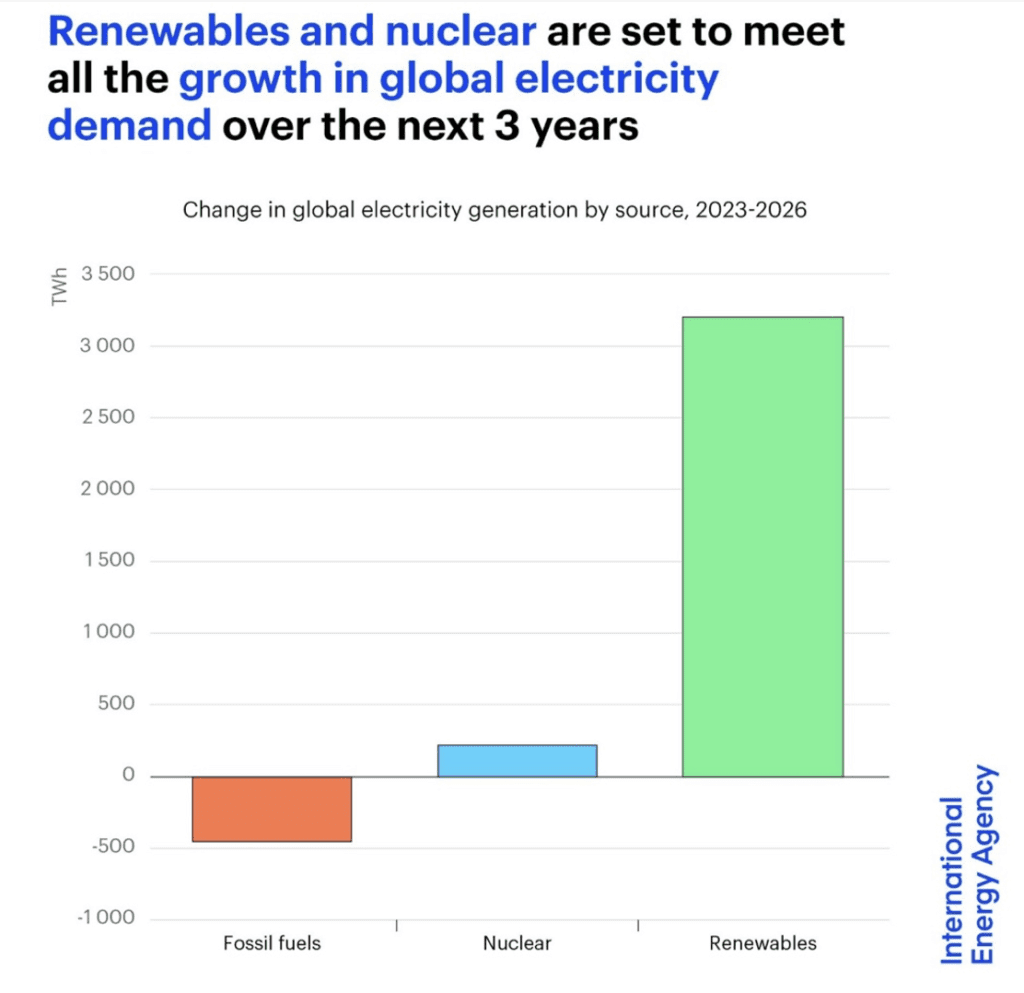

High-emitting energy businesses are falling to their more efficient energy competitors such as wind and solar.

The chart below shows the outcome in the power sector of the next three years from the typically conservative IEA.

Energy investors should be sceptical about funds and investment houses and companies such as oil and gas firms and utilities who drift to transient political preferences over fundamental energy efficiencies and trends.

As the IEA report on the energy transition notes, over the long-term oil and gas returns (6-9% per year) are no larger than renewable energy investments, and they have been historically riskier.

They now also hold existential risk to be added to that equation. Spreadsheets and models need to be upgraded.

The energy business is a long-term and scientifically grounded game: the moves of OPEC and incumbent supporters and investments funds that cling to their business model will form short chapters in the far bigger Book of World Energy.

Incumbents and their backers in investment funds and capital lending are raising the risks of loss to a far higher level – mainly through a lack of imagination, not recognising energy is a far larger, longer and more technically demanding game than just burning oil and gas.