This week, reports[i] have emerged of bp’s CEO Murray Auchincloss latest U-turn regarding bp’s transition strategy: the company has scrapped its previous relatively ambitious target of reducing oil and gas production by 25% by 2030 (vs 2019). Bp had made some headway towards this goal, which would have amounted to a reduction in volumes of 13% in 2030 compared to its output in 2022.

bp’s pivot will increase investors’ exposure to transition risk

The company’s return to its oil and gas roots will likely see the sanctioning of potentially large, high-cost projects – exactly the type which will put investor capital at risk. Bp recently sanctioned[ii] the massive Kaskida deepwater oil field in the Gulf of Mexico, which we highlighted in Paris Maligned II (Table 1) as the largest upcoming project at risk under a moderately paced transition (captured by the IEA’s APS/1.7˚C scenario).[iii] The company has also indicated that it will likely sanction Tiber in 2025, another deepwater oil field which we assess to be at risk under a moderate transition scenario.[iv] Reports this week indicate that bp is set on further expansion in the Middle East, with new production in Iraq[v] and potential re-developments of fields in Kuwait.

Despite what these sanctioning decisions would suggest, Auchincloss has been adamant that he “is not really thinking about production,” but rather about “cash flow and returns.”[vi] If this is the case, why is the company sanctioning new, high cost, long lifespan assets? Is investing in new, risky, long-term oil projects really the most prudent use of company cash flows, or should it instead be returned to shareholders? These are the sorts of questions which investors must ask in the face of this shift in strategy.

bp’s management has struggled to appease investors who remain bullish on oil and gas…

The last two decades have seen bp struggle to carve out a decisive strategy for itself. Its early 2000s rebrand to “beyond petroleum” was reversed about a decade later. Bernard Looney, the last CEO, tried again, laying out a relatively ambitious transition strategy which incorporated cuts to oil and gas production and a renewed focus on renewable energy. Auchincloss appears to be orchestrating the company’s second strategic reversal: alongside the commitment to new oil and gas, the company is pressing pause on renewables, having sold off the US onshore wind business[vii] and paused new offshore wind projects.[viii]

It is fair to say that the markets have not rewarded oil and gas companies like bp who have pursued diversification away from oil and gas; they have arguably been even less keen on companies transitioning to renewables. Corporate leadership has struggled to balance competing expectations and sentiments their investor base, many of whom, particularly in North America, do not duly recognise the magnitude (or sometimes even the existence) of transition risk and thus have not rewarded companies like bp who plan for reduced production (Navigating Peak Demand explores this in more detail).

Yet despite decades of deliberation by oil and gas companies as to their role in the future energy system, the energy transition is accelerating at pace. In some respects, it appears that the decision has been made: the oil and gas industry accounts for only about 1% of global clean energy investment[ix] – even companies who wish to transition may well have missed the boat. What is imperative for the industry now is that companies protect shareholder returns as they continue to service a shrinking market; expanding production with new, risky endeavours is extremely unlikely to be in long-term interests of shareholders.

… though even this cohort should question the prudency of this pivot

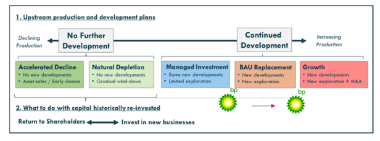

Details of bp’s revised production strategy have yet to be announced, but the initial reports suggest that the company is shifting away from the more managed investment case that we have assessed bp to be following previously and towards one which of increasing oil and gas expansion (Figure 1).

Figure 1: Potential shift in bp’s upstream strategy

Sources: Carbon Tracker, exhibit first published in Navigating Peak Demand, bp Company Profile

This should give pause even to those who are bullish on the future of the Upstream industry: core company strategy is not easily reversible, especially in an extremely technical field like oil and gas. Under Looney, bp cut around 15% of its workforce, including a significant portion of its exploration team – geologists, engineers, and scientists – whose numbers fell to less than 100 from 700 in previous years.[x]

Investors must ask where the capabilities for these new exploration and development drives in Iraq, Kuwait and the Gulf will come from? Is this new expansionary strategy credible, particularly given bp’s chequered history on safety and operational performance? Will this strategy last, or does another u-turn await as market fundamentals increasingly recognise that oil demand is in permanent decline?

Investors with mandates to take climate impact into account will need to square this change with their portfolio targets

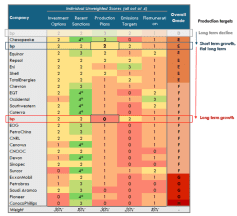

In March, we published Paris Maligned II, which ranked the climate impact reduction plans (or ‘climate alignment’) of 25 of the world’s largest oil and gas companies. bp topped the ranking table as the only company to be graded a D, on a possible scale of A-H.

Full details of bp’s new production guidance have yet to be released, but if the company has pivoted to pursue growth, the impact on its score will be, needless to say, negative. The question remains – how negative? If it’s a short-term growth target, with intentions to hold production flat in the longer term, bp’s grade would fall from a D to an E (Figure 2). However, if its new guidance is for long term growth, then bp’s ranking would plummet to an F, landing it far below its European peers.

Figure 2: Combined alignment assessment (Scale from A-H); updated for potential BP guidance

Notes: exhibit first published in Paris Maligned II, see report for full methodology. If bp would target production growth in the short term and not disclose its long term (2030+) production plans (which would seem less likely as the company has historically published longer term guidance) it would receive a score of 1.

Once bp publishes their updated production guidance, investors with investment mandates related to climate change and/or portfolio decarbonisation targets will need to assess whether the company meets their inclusion criteria. Moreover, the move calls into question the credibility of the bp’s emissions targets. Reuters reports that “The company continues to target net zero emissions by 2050.”[xi] Investors engaging with bp will need to ask how this strategic change squares with this net zero ambition? Are the company’s 2030 emissions reduction target still remotely feasible? What changes will the company implement to ensure these targets are met?

Details will be become clearer at bp investor day next year, but for now we can say that the move is only likely to heighten the risks to the company’s investors and the climate.

[i] Story was reported by Reuters. It has not been confirmed by company at time of writing. https://www.reuters.com/business/energy/bp-drops-oil-output-target-strategy-reset-sources-say-2024-10-07/

[ii] https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-gives-go-ahead-for-sixth-operated-hub-kaskida-in-the-us-gulf-of-mexico.html

[iii] https://www.iea.org/reports/the-oil-and-gas-industry-in-net-zero-transitions/executive-summary

[iv] https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-second-quarter-2024-results-qa-transcript.pdf

[v] https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-and-iraq-agree-to-explore-redevelopment-in-kirkuk.html

[vi] https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-second-quarter-2024-results-qa-transcript.pdf p. 14

[vii] https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-to-divest-operating-us-onshore-wind-business-as-it-focuses-onshore-renewables-in-lightsource-bp.html

[viii] https://www.reuters.com/business/energy/bp-halts-hiring-slows-renewables-roll-out-win-over-investors-2024-06-27/

[ix] https://www.iea.org/reports/the-oil-and-gas-industry-in-net-zero-transitions/executive-summary

[x] https://www.reuters.com/article/business/bps-oil-exploration-team-swept-aside-in-climate-revolution-idUSKBN29U00B/#:~:text=Its%20geologists%2C%20engineers%20and%20scientists,exploration%20team%20since%20Looney’s%20arrival.

[xi] https://www.reuters.com/business/energy/bp-drops-oil-output-target-strategy-reset-sources-say-2024-10-07/