Evaluating Automotive Transition Strategies

Electrification of the passenger vehicle fleet is inevitable. To be relevant in a decarbonised future economy, automakers must effectively manage the transition of their product lineups from internal combustion engine (ICE) vehicles to battery electric vehicles (BEV). With that said, climate-engaged investors cannot expect automakers to immediately switch to 100% EV sales ‘overnight’ for several reasons including:

- Manufacturing Assets – Sunk investments in vehicle manufacturing facilities (PP&E) must be repurposed and retooled to build EVs on dedicated electric vehicle architecture.

- Research and Development – OEMs (Automakers) must invest over an extended period in electric vehicle technology and architecture to produce competitive BEV products.

- Supply of components and materials – automotive supply chains are notoriously complex, and OEMs must secure supply chains for components, including batteries, and materials for the on-going manufacture of BEVs.

However, automakers need a pragmatic strategy to transition to an electric fleet or face obsolescence. This blog compares 2 OEMs, Toyota and BMW, their strategies in the automotive transition, and what it means for the wider industry.

End of the ICE Age – Demand for combustion engine vehicles melting away

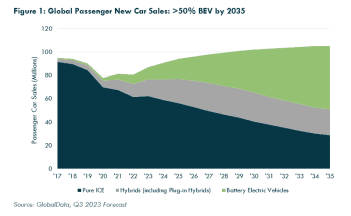

Despite a recent slowdown in global BEV sales growth (note: not a decline in year-on-year sales), the future of the passenger car sector is battery electric. According to GlobalData, BEV sales globally will make up at least 50% of the new car market in 10 years’ time, up from ~15% in 2024 (Figure 1). Of course, this is to the detriment of ICE vehicle market share.

At present, China is a clear leader in BEVs with its domestic OEMs having learnt how to build high quality cars through their joint venutures with Western partners, whilst supported by a long-term national industrial strategy to develop electric vehicle technologies, including batteries. BYD is now the largest BEV manufacturer in the world, overtaking Tesla in just 5 years. Incumbent players, including Toyota and BMW, must consider how their transition strategy will play out in a BEV market led by China and its domestic OEMs.

OEM Powertrain Strategies

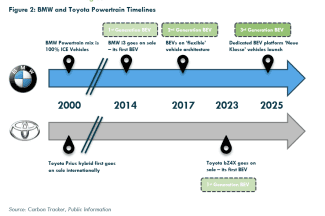

Toyota was an early pioneer in electrification, employing hybrid technology in a vehicle in the early 2000s (Figure 2). This bestowed the world’s largest automaker with early ‘green’ credentials; a reputation it still has today, at least by the general consumer. However, Toyota never really improved on this early lead in the automotive transition to zero tailpipe emissions, instead refining its hybrid technology and depreciating/ amortising the sunk development costs over many years to improve the profit margins on these vehicles.

More than 20 years after the first Toyota hybrid vehicle was sold, the company started selling its first BEV. The begrudging addition of a BEV in Toyota’s product offerings occurred after the company’s attempts to sell hydrogen fuel cell (FCEV) passenger vehicles to the mass market ultimately failed. Today, Toyota executives quote the ‘multi-pathway’ approach to emissions reduction by offering consumers hybrids, plug-in hybrids, BEVs and FCEVs. However, this strategy implies splitting capital expenditure and development costs across numerous powertrains; an inefficient use of capital. Toyota are already behind on the development of BEVs, meaning that the company is effectively selling its first-generation BEV. Surely Toyota’s ‘green reputation’ is tainted if it is only deploying its first-generation BEV and is relying on vehicles with ICEs to meet climate goals. Toyota has become a laggard in BEVs and actively lobbies against stricter emissions legislation.

Meanwhile, in 2025 BMW will launch its class of third-generation BEVs built on a new dedicated electric-only platform, aptly called ‘Neue Klasse’. While Toyota were bringing hybrids to market in the early 2000s, BMW only sold purely ICE vehicles but have since caught up and overtaken Toyota in terms of electrification (Figure 2). BMW have used hybrids, in particular mild-hybrids and plug-in hybrids in their product offerings to meet stricter emissions legislation, especially in Europe, but surprised competitors with the release of the i3 for model year 2014; the company’s first BEV. This innovative vehicle sold well reaching almost a quarter of a million sales before its production run ended in 2023. Concurrently, from 2017 BMW started using a ‘flexible’ vehicle architecture to help electrify its product lineup and offer electric versions of ICE vehicle models; the company’s second-generation of BEVs. About 10 years after the launch of the i3, BMW will unveil its third generation BEV platform ‘Neue Klasse’.

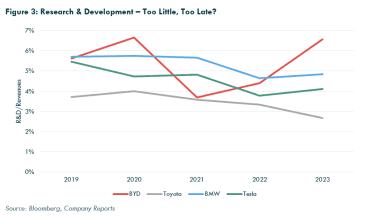

Research and development (R&D) is a proxy for a company’s investment into the future. In general, a company deploying significant resources into R&D now will increase the likelihood of developing the innovative products of the future. By comparing R&D, Toyota has the lowest R&D to revenues ratio (Figure 3). Toyota’s R&D activities will be spread across multiple powertrains, such is their strategy, compared a pureplay BEV manufacturer like Tesla. In comparison, on average over the last 5 years, BMW’s R&D to revenues ratio is ~2 percentage points higher than that of Toyota.

Is Toyota’s foray into BEVs too little, too late?

Toyota has been scrutinised for being cautious about going ‘all in’ on BEVs, instead focussing on hybrid technology. With the recent deceleration in BEV demand, Toyota has capitalised on this and increased sales of their hybrid vehicles, ultimately being rewarded with a 17% rise in operating profits in Q1 2024. On the face of it, Toyota’s strategy looks well placed…for now.

But as Figure 1 shows, demand for vehicles with a combustion engine (including hybrids) peaked in 2017. Growth in hybrid sales is expected to plateau at around 20 million vehicles per year out to 2035, meanwhile new BEV sales could grow with a compound annual growth rate of 13% (2024-2035). Investors should ask why a leading company is not chasing the growth area of a market.

A good litmus test for the financial/market opportunity of a technology is the arrival of new entrants. Over the last 20 years there has been an influx of pureplay BEV companies, like Tesla and more than one hundred others, most of which from China. It is quite likely that only a handful of these BEV startups will survive, but the message is clear – the future opportunity is large enough for startups to enter the market. Are hybrids the future? Count the number of pureplay hybrid electric vehicle startup automakers…. Zero. Hybrids are likely a transition bridge to nowhere.

China Centric Car Market – BEVs stymie market share declines

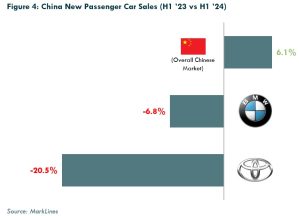

China is the single largest car market globally, with annual new car sales of ~30 million vehicles, and is therefore critically important for major automakers. China also leads the world in terms of BEV market share, making up approximately a quarter of the country’s annual new car sales. The overal Chinese market grew by 6.1% between H1 ’23 and H1 ’24 (Figure 4), but with the rise of domestic BEV players, foreign automakers have had a tough first half of the year, with sales declining 6.8% and 20.5% respectively for BMW and Toyota. The clear peril of this for an established automaker is that it misses growth in BEVs and is constantly battling hybrid developments from existing competitors.

BMW have been more invested in BEV developments, and now have 15% of their global sales as BEVs versus only 3% of Toyota. In the first half of this year, BMW sold almost 2.5x the number of BEVs in China than Toyota did, helping to minimise market share losses. Around 20% of all BMW sales in China were BEVs, compared with about 4% of Toyota sales being BEVs.

But the wider trend is causing all automakers (except Chinese ones) to lose out on growth in the China market as their technology developments have not kept pace with China’s BEV pivot.

Emissions Compliance – The Cost of Carbon

Emissions legislation has been the driving force in the electrification of the vehicle fleet and reducing carbon from tailpipe emissions. Automakers have a strategy choice on how they will comply with emissions legislation: 1) invest capital in electrification including batteries and/ or 2) buy emissions credits from other automakers. Emissions non-compliance comes with penalty fines and reputational risk.

BMW has managed to comply with emissions legislation by successfully deploying hybrid and battery electric vehicles and will pivot to a larger share of BEV sales to lower fleet average emissions as emissions legislation becomes stricter (for example, ‘Neue Klasse’ will be released in 2025, when EU fleet average CO2 targets become 15% stricter versus 2020/21).

Toyota’s mostly hybrid strategy will only get the company so far in complying with longer term emissions legislation. To fill a likely ‘emissions compliance gap’ that is forming, Toyota’s North America CEO admitted the company would rather buy carbon credits from other automakers than ramp up BEV production. Buying carbon credits is a waste of capital that could have been used in the development of BEVs, software etc. Toyota is effectively subsidising the BEV development costs of other manufacturers by buying carbon credits from its competitors.

For an automaker, the cost of not decarbonising is falling further behind Chinese BEV competitors. Recently BMW’s CEO called for slower EU policy mandates on the BEV transition and protection for e-fuel/synthetic fuel developments. BMW and Toyota also recently signed an agreement towards the ‘advancement of a hydrogen society’. These distractions will only hinder a company that is serious about decarbonising its vehicle fleet.

Emissions Reporting Risks

Investors are becoming increasingly sustainability-focused, and, in the EU at least, are now subject to mandatory reporting of the carbon intensity of the companies they invest in.

As Carbon Tracker’s report Oil Companies in Disguise – 2024 Edition discusses, there is an industrywide gap between automakers’ real annual carbon emissions and what they are publicly reporting, which can be traced mostly to underestimates of vehicle lifetime use. At the time of report publication, both BMW and Toyota had a ‘carbon gap’ i.e. the difference between OEM declared and calculated estimated emissions, in their most recent sustainability reports.

Toyota significantly improved the accuracy of its emissions reporting over the last year. It increased its self-reported CO2 emissions by 45% and applied a more accurate vehicle lifetime-use methodology from SBTi. The sharp upward revision implies that the company’s previous sustainability reports used inaccurate carbon data. Investors should be wary of the potential hidden embedded emissions in companies they invest in.

To win back environmentally conscious stakeholders, an accelerated shift to fully electric powertrains remains one of the best ways for an automaker to show it is reducing emissions. As long as an OEM, like Toyota, product strategy remains linked to internal combustion engines and hybrids, fears of further inaccurate emissions reports and hidden embedded emissions will remain.

Conclusion

Converting the vehicle fleet to 100% BEV will take time. OEMs must adapt their product offerings not only to meet emissions goals, but also to remain relevant in a decarbonised, electric and inreasingly China-led automotive market. Hybrids, whilst offering some efficiency gains, are a technology of the past and represent a stagnant part of the powertrain sales mix out to 2035, with all the sales growth for BEVs.

An automotive strategy linked to vehicles with a tailpipe comes with inherent risks:

- Product risk – ICE products will become obsolete in a decarbonised economy, leading to potential stranded asset risk of ICE PP&E.

- Emissions risk – potential for tailpipe emissions legislation non-compliance leading to penalty fines or wasted capital buying carbon credits.

- Reporting risk – inaccurate emissions reporting in company statements could hide the true carbon footprint of automakers, impairing investors to make informed sustainability investment decisions.

- Reputational risk – OEMs could have their reputation damaged if they are seen to be laggards in the transition

For BMW, Toyota and for any incumbent ICE manufacturer, these are all risks that will become more acute when considering the pace of the transition. The laggards of the industy still have time to alter course, invest heavily in BEVs, and take leadership in future technology, but the window is closing as competitors (old and very new) position themselves to take significant market share in a zero-emission automotive future.

Disclaimer

Carbon Tracker is a non-profit company set up to produce new thinking on climate risk. The organisation is funded by a range of European and American foundations. Carbon Tracker is not an investment adviser, and makes no representation regarding the advisability of investing in any particular company or investment fund or other vehicle. A decision to invest in any such investment fund or other entity should not be made in reliance on any of the statements set forth in this publication. While the organisations have obtained information believed to be reliable, they shall not be liable for any claims or losses of any nature in connection with information contained in this document, including but not limited to, lost profits or punitive or consequential damages. The information used to compile this report has been collected from a number of sources in the public domain and from Carbon Tracker licensors. Some of its content may be proprietary and belong to Carbon Tracker or its licensors. The information contained in this research report does not constitute an offer to sell securities or the solicitation of an offer to buy, or recommendation for investment in, any securities within any jurisdiction. The information is not intended as financial advice. This research report provides general information only. The information and opinions constitute a judgment as at the date indicated and are subject to change without notice. The information may therefore not be accurate or current. The information and opinions contained in this report have been compiled or arrived at from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made by Carbon Tracker as to their accuracy, completeness or correctness and Carbon Tracker does also not warrant that the information is up-to-date.