Key Resources

Related Report

Response to Exxon: An Analytical perspective

Read MoreKey Quotes

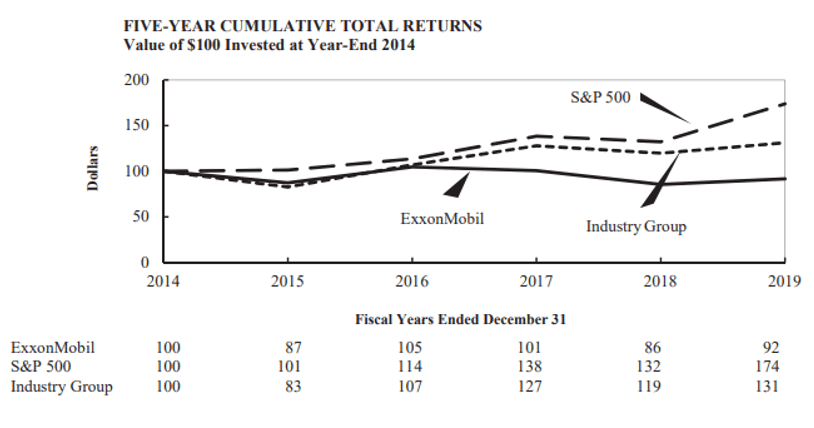

Between 2014 and the end of 2019, ExxonMobil ‘s return to shareholders was negative 10%.

In September 2014, Carbon Tracker published a report on ExxonMobil. It highlighted that Exxon’s long-term outperformance of the market and its peers appeared to be coming to an end. The cause of this was Exxon’s overinvesting in capital intensive, high cost, high carbon projects, especially oil sands. It concluded that Exxon’s returns were likely to deteriorate further unless it changed its strategy.

Exxon didn’t change its strategy and someone who invested in ExxonMobil at the time of the report would have been better off putting their cash under the mattress instead.

Source: ExxonMobil’s Financial Statements and Supplemental Information for 2019

Key Findings

In the past year, ExxonMobil has dropped out of the S&P 500 “Top ten” stocks and been removed from the Dow Jones Index. Quite embarrassing occurrences for what used to be one of the largest and most highly rated quoted oil companies in the world.

Up until 2007, Exxon had an enviable track record, delivering shareholder returns above both its peers and the wider market. But between 2007 and 2014, those returns started to deteriorate. And between 2014 and 2019, shareholders actually lost money. It even underperformed its oil major peer group suggesting an Exxon-specific rather than industry problem.

Carbon Tracker believes that a major reason behind this poor performance was that Exxon overinvested in high cost assets in order to chase growth. The consequential ballooning in its capital base and its operating costs were a major factor behind the collapse in its return on capital. Its shareholder returns followed suit.

Despite this escalation in spending, which led to its upstream (production) capital employed nearly tripling between 2007 and 2019, its proven reserves hardly changed and its production actually fell. Hardly a successful “growth” strategy, especially when accompanied by such poor shareholder returns in the past five years.

Carbon Tracker pointed out the risks to Exxon’s aggressive development programme in a report in early 2014. It showed that Exxon’s bet on high cost, low return assets such as heavy oil (including tar sands) and LNG (Liquified Natural Gas) had already started to depress the group’s return on capital. Its portfolio of future development projects was heavily skewed to such assets.

The damage Exxon’s “growth” strategy caused to investor returns is astonishing. Between 2007 and 2019, Exxon delivered shareholder returns (capital gains plus dividends) of 10% in total, less than 1% a year. In contrast, Chevron shareholders saw returns double, equivalent to an annual return of 6% a year. In aggregate, Exxon shareholders would have been better off to the tune of over US$400 billion if they had invested in Chevron instead.

Carbon Tracker believes Exxon should exercise stricter capital discipline and abandon its growth strategy. It should be focusing on high return, low cost developments in order to boost its return on capital. Chasing growth for growth’s sake has proved to be a flawed strategy that has damaged shareholder returns and – ironically – failed to produce growth in reserves or production.