Key Resources

Press Release

Press Release

Read MorePetro-Provinces at Risk

Petro-Provinces at Risk

Read MoreKey Quotes

True Oil & Gas Value in Canada and Beyond

Despite a decline in the share of free cashflow allocated to upstream oil and gas capital expenditures in recent years, companies’ narrative on energy demand and production growth remains bullish. Several large Canadian financial institutions and provincial economies are highly exposed to Canadian oil and gas, underscoring the need for a rigorous assessment of value.

This report explores whether investment in new upstream projects risks eroding Canadian oil and gas value. It benchmarks Canadian firms against global peers to determine relative positioning and provide a view on risk exposure in a worldwide context.

“One of the core questions investors should be asking of oil and gas corporates is the extent to which new projects are value-additive. Potential new projects put up to ~30% of Canadianoil and gas value at risk under a fast-paced transition scenario, roughly triple the size of potential upside under a slow-paced transition.”

Key findings

- New projects place up to ~30% of Canadian oil and gas value at risk under a fast-paced transition scenario where prices fall to $30/bbl.

- New gas projects erode value under a moderate-paced transition seeing gas equivalent prices of $50/bbl.

- Canadian oil and gas production growth represents a high-risk, low-reward strategy.

- New projects expose Canadian companies to greater upstream value-at-risk than most global peers.

- Stakeholders (investors, lenders, regulators, and policymakers) should take action to mitigate wide-ranging risks from new oil and gas projects.

What the data shows

Investment in new projects does not automatically create value. Across different transition pathways, higher spending on new Canadian oil and gas projects can reduce net present value (NPV), particularly under slower-paced transition scenarios.

Level of investment in new oil and gas projects and transition pace on Canadian sector NPV.

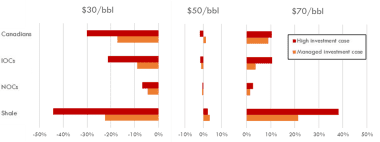

A peer comparison across a range of commodity price scenarios shows that Canadian oil and gas companies are more exposed to value erosion from new upstream investment than integrated oil company and national oil company peers, especially under fast-transition conditions.

Relative NPV of Canadian, IOC and NOC portfolios under different investment levels and price scenarios.

Sources: Rystad Energy, CTI analysis

What this means

For investors

- Engage Canadian oil and gas firms to disclose medium- (and ideally long-) term production and capex plans.

- Request disclosure of break-even commodity prices, expected returns, and modelling assumptions for new projects.

- Sense-check project assumptions and engage companies on value-at-risk under faster transition scenarios.

- Use this report’s findings to assess the financial and credit profile of Canadian oil and gas companies and guide investment decisions.

For policymakers and regulators

- Regulators should stress test the financial system and require financial institutions to stress test portfolio exposure to fossil fuel prices grounded in realistic transition scenarios.

- Require oil and gas firms to disclose risks to future cashflow under range of transition scenarios.

- Policymakers should review fossil fuel subsidies considering heightened cashflow and value risk.

- Consider withdrawing public financing for new oil and gas assets, including pipelines and CCS, that appear premised on the notion that upstream growth is value-additive.

- Question the economic rationale for new exploration licences, given elevated cashflow risk.

- Support infrastructure delivering affordable, secure, clean energy; prioritise R&D and workforce upskilling aligned with climate goals.

Download the report

Dive into the full report for more insights on whether investment in new upstream projects risks eroding Canadian oil and gas value. Use the download button at the top of this page.

This report is one of a two-part series analysing the value of Canadian oil and gas amid the unfolding energy transition. The second report evaluates how the energy transition could affect provincial government revenues, outlining key policy developments and sectoral risks. It also examines challenges in scaling up CCUS and highlights opportunities to diversify tax bases through transition-resilient sectors. Read Petro-Provinces at Risk here.