Key Resources

Press Release

Exchanges carrying 3 times more carbon reserves than can be burned under Paris

Read MoreInfographic

Launch Event

Unburnable Carbon: are the World’s Financial Markets Carrying a Carbon Bubble? A Decade on

Read MorePolicymaker Brief

Key Quotes

Over $1 trillion of oil & gas assets risk becoming stranded as a result of policy action on climate and the rise in alternative energy sources.

The majority of this unburnable carbon is held by companies listed in just a handful of global financial centres.

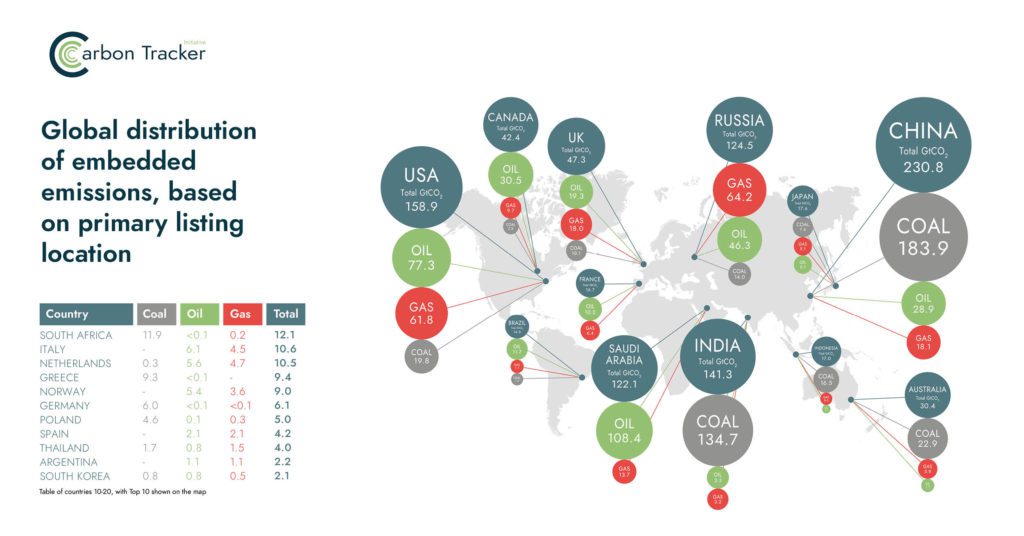

Unburnable Carbon: Ten Years On finds that the majority of embedded emissions are listed on the stock exchanges of China, USA, India, Russia and Saudi Arabia where, with the exception of the USA, emissions are dominated by the partial listings of state-owned companies.

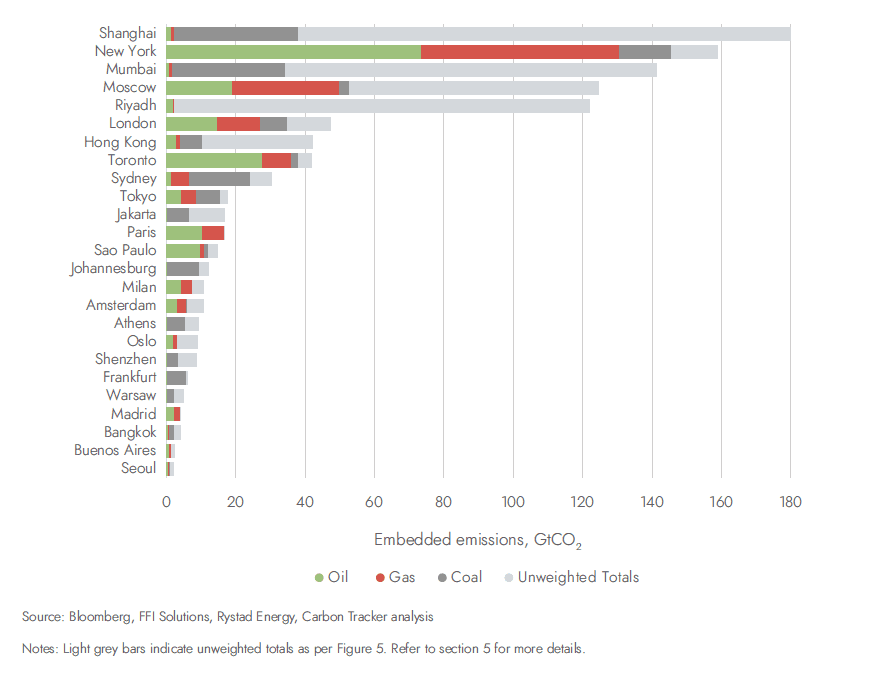

Figure 1: Emissions embedded (GtCO2) in the reserves of listed and partially-listed companies, by financial centre of primary listing, free-float weighted.

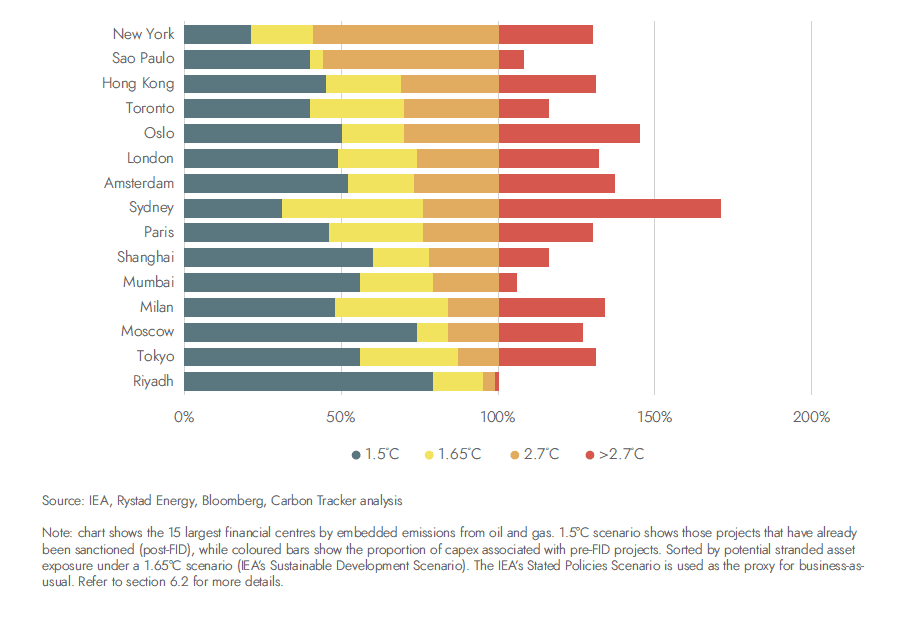

The report quantifies the stranded asset risk exposure for the oil and gas assets and finds over $1 trillion of oil & gas assets risk becoming stranded, and the majority, some $600bn, is held by listed companies. In absolute terms, this stranded asset risk is concentrated in the financial centres of New York, Moscow, London, and Toronto.

Figure 2: Stranded asset exposure by financial centre shown as upstream oil & gas capex by financial centre, 2021-2030, as % of business-as-usual capex (2.7°C).

Figure 3: Global distribution of embedded emissions, based on primary listing location

Key Findings

- To limit warming to 1.5°C, 90% of fossil fuel reserves must remain in the ground as unburnable carbon.

- The majority of this unburnable carbon is held by companies listed in just a handful of global financial centres.

- Adjusting for state/restricted ownership reveals New York, Moscow, Toronto and London as the financial centres with the highest embedded emissions from upstream oil and gas companies over which investors have influence.

- Despite some having set “net zero” goals, these financial centres enable the ongoing activities of the incumbent fossil fuel industry, in many cases to a far greater degree than national reserves.

- Listed companies are exposed to significant transition risk.

- Energy transition risks apply not just to producers, but across the full oil and gas value chain (e.g. refiners) as well as a wide range of different financial services providers.

- Policymakers must view the facilitation of new fossil fuel as contrary to achieving national climate goals.