Key Resources

Webinar Recording (Asia-Pacific/Europe Session)

Webinar Recording (Asia-Pacific/Europe Session)

Webinar Recording (Americas Session)

Webinar Recording (Americas Session)

Press Release

Press Release

Read MoreLaunch Webinar (Europe/Asia Session)

Oil Companies in Disguise: Are Investors Mispricing Automotive Climate Risk? (Asia-Pacific/Europe Session)

Read MoreLaunch Webinar (Americas Session)

Launch Webinar (Americas Session)

Read MoreKey Quotes

Reporting gaps reveal the true carbon intensity of automotive investments

Passenger vehicles remain the largest and most durable source of global oil demand. Every internal combustion engine (ICE) or hybrid vehicle sold locks in years of future fossil fuel consumption, making automakers structural enablers of the oil system. Yet current emissions reporting frameworks systematically understate the scale of this exposure.

This report analyses 17 of the world’s largest automakers and identifies a systemic “Carbon Gap” between reported Scope 3 Category 11 emissions and estimated real-world lifecycle emissions. Across the sector, Carbon Tracker estimates a median reporting gap of 33%, driven by differences between corporate reporting assumptions and real-world vehicle emissions. Adjusted emissions estimates suggest several automakers are as carbon intensive as traditional oil and gas companies.

Key findings

- Automakers are structural drivers of oil demand. Each ICE or hybrid vehicle sale locks in 10-20 years of future fuel consumption and associated emissions.

- Scope 3 Category 11 reporting systematically understates real-world emissions exposure due to conservative mileage assumptions, unrealistic hybrid utility factors and omission of upstream fuel-production emissions.

- Across 17 global automakers, Carbon Tracker estimates a median 2024 “Carbon Gap” of 33% between reported and estimated real-world emissions.

- Differences in reported emissions are not solely driven by vehicle mix; disclosure assumptions and reporting methodologies also materially affect reported outcomes.

- Hybrid-heavy transition strategies risk prolonging oil demand and increasing stranded asset exposure as markets accelerate towards full electrification.

- BEV-focused manufacturers are structurally reducing oil exposure, while laggards remain tied to long-term fossil fuel dependency.

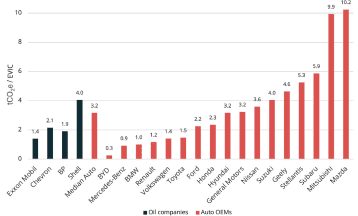

Sector value carbon intensity – oil & gas versus automotive (2024)

Several automakers exhibit carbon intensity levels comparable to, or higher than, traditional oil and gas companies when measured against enterprise value.

What the data shows

Differences between reported and estimated emissions are primarily driven by discretionary assumptions around vehicle lifetime mileage, hybrid usage and emissions accounting boundaries.

The findings suggest investors may be relying on emissions disclosures that are not directly comparable across issuers due to differing assumptions around vehicle lifetime mileage, hybrid usage and emissions boundaries. This may contribute to the underpricing of carbon exposure, stranded asset risk and future regulatory liabilities.

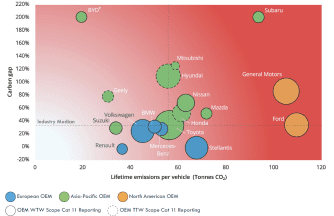

Carbon gap versus lifetime emissions per vehicle (2024)

The bubble chart highlights leaders and laggards across major automotive manufacturers, showing that higher vehicle emissions do not necessarily correspond with stronger alignment to decarbonisation pathways.

Recommendations

For investors:

- Scrutinise the assumptions underpinning Scope 3 Category 11 disclosures.

- Prioritise BEV sales share as a core transition metric.

- Assess exposure to long-term ICE and hybrid dependence.

- Consider carbon intensity metrics alongside reported emissions disclosures when assessing transition risk.

For regulators and standard setters:

- Strengthen standardisation of automotive Scope 3 reporting.

- Improve transparency around vehicle lifetime and real-world emissions assumptions.

For automakers:

- Accelerate BEV deployment.

- Align emissions reporting with real-world vehicle performance.

Download the full report to explore the methodology, automaker-level analysis and implications for investors, regulators and policymakers.