Key Resources

Press release

Flying blind: The glaring absence of climate risks in financial reporting

Read MoreRelated article

Financial Times Exclusive

Key Quotes

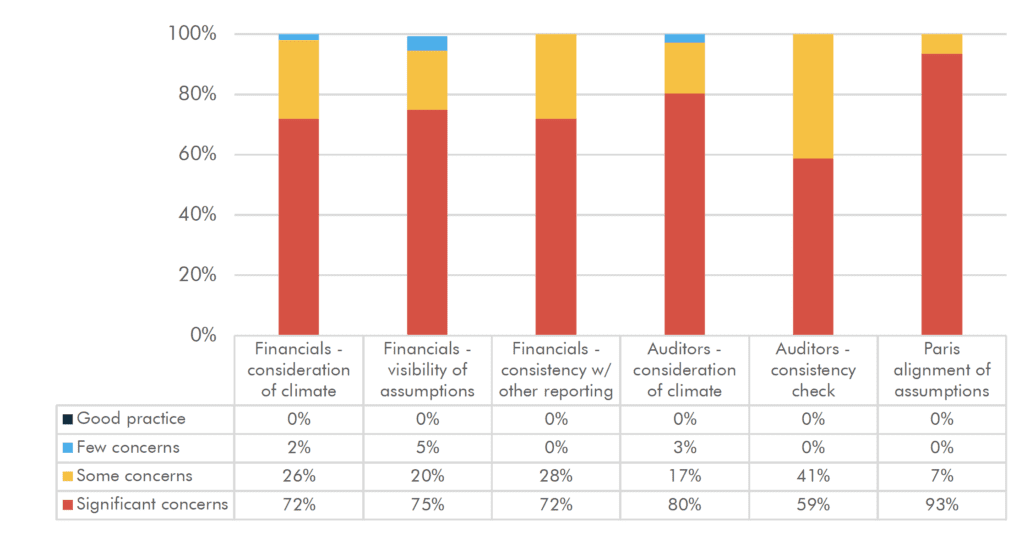

Investors are Flying Blind as over 70% of reviewed companies and 80% of auditors fail to disclose climate-related risks in the financials

This report examines whether 107 publicly-listed carbon-intensive firms (and their auditors) considered material climate-related risks in financial reporting. At the same time the study also assesses whether investor concerns about Paris-alignment of assumptions and estimates have been addressed. The study covered a range of sectors: 33% Oil and Gas, 17% Transportation, 13% Utilities, 7% Cement, 7% Consumer Goods and Services, and 23% Other industrials (including mining, chemicals and steel).

In 2019 and 2020 global accounting[2] and auditing standard-setters clarified that material climate-related risks should not be ignored in accounts or in audits. Another concern raised by the report is the lack of consistency across company reporting. 72% of companies showed no evidence of follow through from other discussions of climate risks or emissions targets to their treatment in the financial statements, or explained any differences.

Despite significant financial risks faced from the climate crisis, and net-zero pledges made by many we found little evidence that companies or their auditors considered climate-related matters in the 2020 financial statements.

Figure 1: Overall results – considerations of climate matters in financial statements and audit reports

Source: Carbon Tracker and CAP team analyses

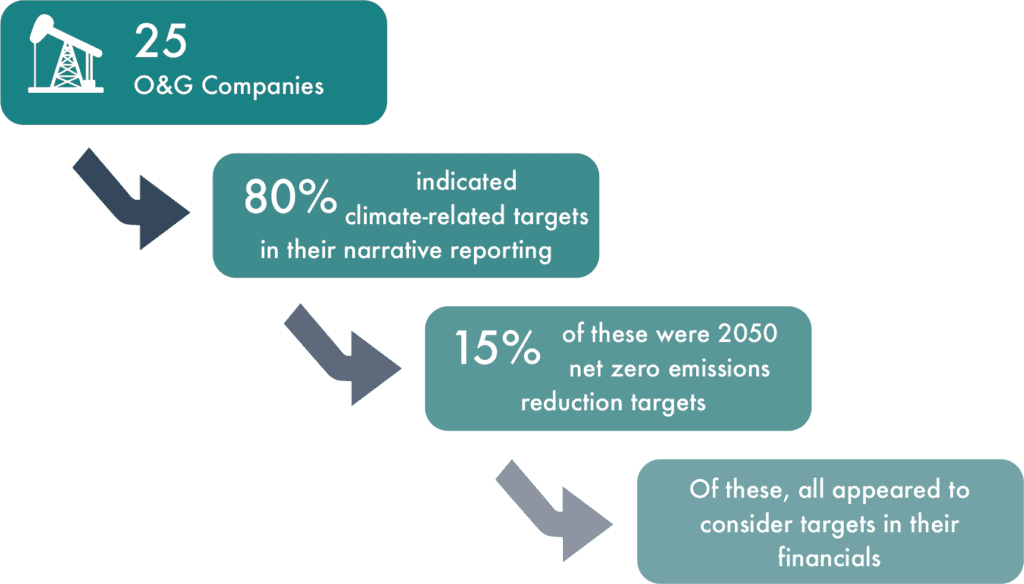

Compared to other sectors profiled, oil and gas companies provided the most evidence of, and transparency around, consideration of climate-related matters in their financials and audit reports. These companies were the most visible in terms of providing/detailing the assumptions used, even if they did not always consider climate in those assumptions, nor align them with preferred Paris outcomes.

Figure 2: Consistency in considering climate targets – O & G companies

Source: Carbon Tracker analysis and graphic

Key Findings

- There is little evidence that companies incorporate material climate-related matters into their financial statements.

- Most climate-related assumptions and estimates are not visible in the financial statements.

- Most companies do not tell a consistent story across their reporting.

- There is little evidence that auditors consider the effects of material climate-related financial risks or companies’ announced climate strategies.

- Even with considerable observable inconsistencies across company reporting (‘other information’ and financial statements), auditors rarely comment on any differences.

- Companies do not appear to use ‘Paris-aligned’ assumptions and estimates.